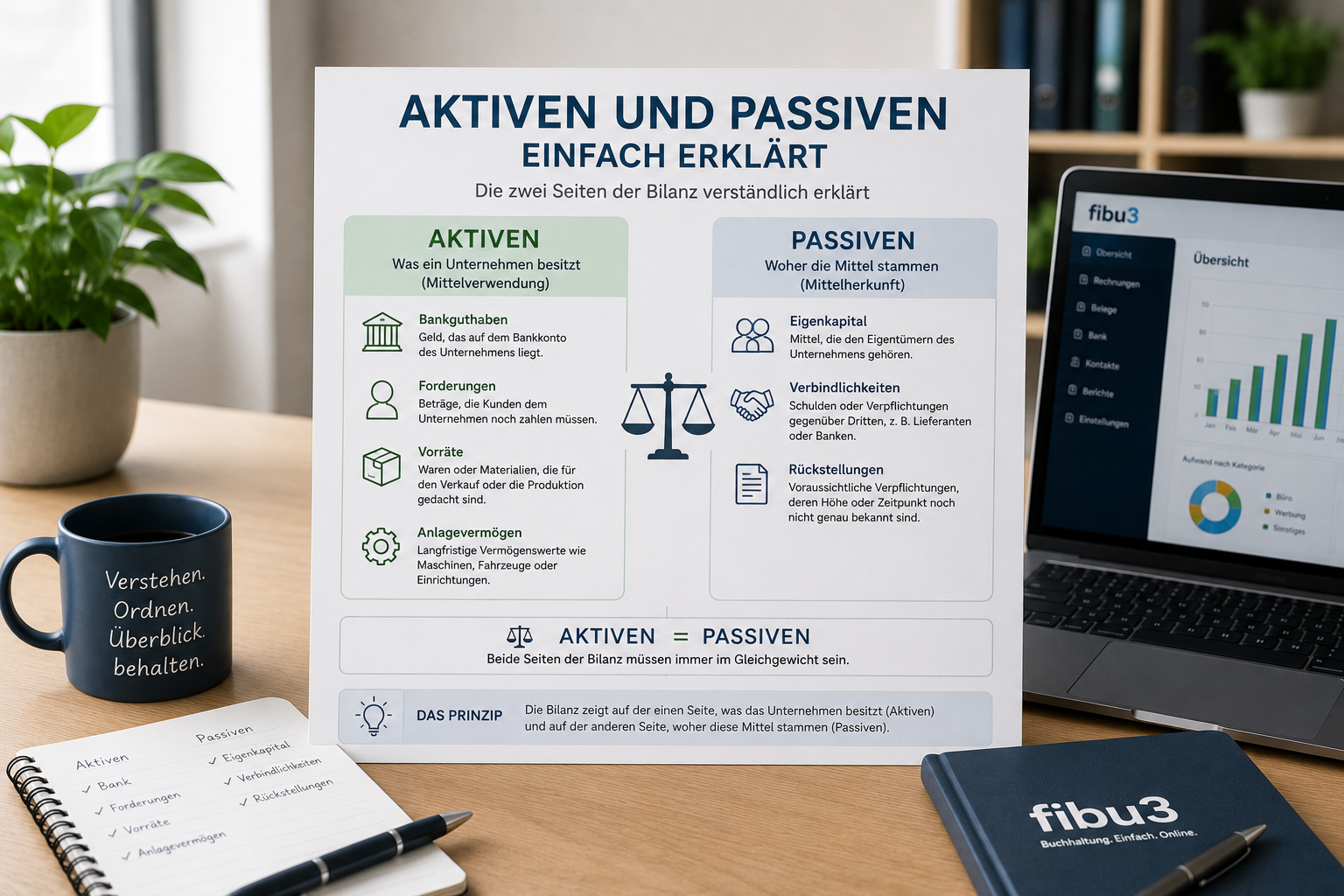

What is double-entry bookkeeping?

Double-entry bookkeeping means, in simple terms, that every business transaction is posted to two accounts: once on the debit side and once on the credit side.

It is called double not because you do the work twice, but because every movement has two sides. If you pay an invoice, your bank balance changes and so does another account, such as an expense or an open payable.

What do debit and credit mean?

Debit and credit are the two sides of a posting. Every posting changes at least two accounts, and that matching movement is what keeps the bookkeeping traceable.

At the beginning, it helps to think less about the words themselves and more about this question: which account increases and which account decreases? The exact direction depends on the account type, but the basic idea always stays the same.

| Business case | Debit | Credit | Explanation |

|---|---|---|---|

| Pay a supplier invoice | Payable or expense | Bank | The liability or expense is recorded and at the same time the bank balance decreases. |

| Buy a laptop via the business account | Asset account for IT/office equipment | Bank | The laptop enters the business and the cash leaves the bank account. |

| Customer pays an open invoice | Bank | Receivable | The money arrives in the bank and the open receivable disappears. |

| Deposit cash into the bank | Bank | Cash | The money stays in the business but moves from cash on hand to the bank account. |

Why do you need double-entry bookkeeping?

Double-entry bookkeeping helps businesses document money movements in a traceable way and see their financial position at any time.

With a simple list of income and expenses, you can see movement, but not the whole picture. Only when you also track assets, liabilities, receivables and expenses do you really see what is still open and how clean the numbers are.

- more transparency around assets and liabilities

- better control over open invoices and payables

- a clean basis for year-end closing and taxes

- easier error detection

- better traceability for the business, fiduciaries and banks

Who needs double-entry bookkeeping in Switzerland?

As a practical rule of thumb, limited liability companies and corporations work with double-entry bookkeeping. For sole proprietorships and partnerships, the answer depends more on legal form, turnover and overall complexity.

Official federal SME information states that sole proprietorships and partnerships with turnover of at least CHF 500,000 in the previous financial year must keep accounts under Swiss Code of Obligations provisions, while smaller businesses keep at least simplified books. For associations, structure and scale also matter.

Is double-entry bookkeeping complicated?

Not necessarily. The basic principle is simple; what often feels complicated is the language around it.

Many people think they first need to memorize every rule. In practice, getting started usually only requires understanding that every posting has two sides and that good software supports the allocation.

A simple real-life example of a posting

You buy a laptop for CHF 1,500 through the business account. An asset account for IT or office equipment increases, and at the same time your bank account decreases by the same amount.

That is exactly why the posting needs two sides: the business now owns a laptop, but there is less money in the bank. The exact account name depends on the chart of accounts, but the principle stays the same.

Which account increases?

The asset account for the laptop or office equipment increases because a new asset enters the business.

Which account decreases?

The bank account decreases because CHF 1,500 leaves the business account.

Why two sides?

Because a posting should always show where the change comes from and where it ends up. That is what makes the movement fully traceable.

Typical mistakes at the beginning

The biggest beginner problems are often not technical but organizational. If you make things more complicated than necessary or wait too long, you lose oversight more quickly.

Trying to memorize debit and credit

It helps more to understand the movement. Which account increases and which decreases is often the better beginner question.

Thinking too abstractly

Many everyday postings are very logical. The fear often comes from the terminology, not from the transaction itself.

Collecting receipts chaotically

If receipts are spread across pockets, inboxes and downloads, every posting becomes more painful than necessary.

Postponing postings

If you only gather everything at quarter end or year end, you create unnecessary follow-up questions.

Forcing everything into Excel

That may work for very simple cases, but with invoices, bank reconciliation and VAT it quickly becomes messy.

Not having a separate business account

As soon as private and business payments are mixed, bookkeeping becomes harder than it needs to be.

Excel or accounting software?

Excel works for very simple cases, but it quickly becomes unclear once invoices, bank movements or VAT enter the picture.

The real difference lies less in the file itself than in the structure: software guides recurring tasks more cleanly, while Excel leaves everything open and therefore also allows more mistakes.

| Aspect | Excel | Accounting software |

|---|---|---|

| Structure | flexible | more structured |

| Workload | more manual work | fewer day-to-day error sources |

| Postings | no built-in support | support for postings |

| Invoices | no integrated invoicing module | integrated processes |

| Bank reconciliation | manual follow-up | clearer reconciliation and better overview |

How does fibu3 help you get started?

fibu3 helps you get started because postings, invoices, quotes and bank reconciliation come together in one interface. That does not make double-entry bookkeeping magically easy, but it makes it much more tangible.

If debit and credit are not second nature yet, assisted posting is usually more helpful than a blank spreadsheet. For smaller companies and self-employed professionals, it is also practical that you can start with up to 40 entries for free.

- assisted posting instead of a blank template

- invoices and quotes in the same place

- more structure instead of bookkeeping chaos

- bank reconciliation without constant tool switching

- a clearer route into day-to-day work

- up to 40 entries for free

In one sentence: double-entry bookkeeping explained

Double-entry bookkeeping means that every business transaction changes two accounts so money movements, assets and liabilities stay traceable.

Checklist: do I already understand the basics?

If you can answer most of these questions with yes, getting started with double-entry bookkeeping is usually less dramatic than it first sounds.

- Do I broadly understand what debit and credit mean?

- Do I know why every posting has two sides?

- Do I collect my receipts properly?

- Do I have a separate business account?

- Am I using a clear structure or software for bookkeeping?

Conclusion: double-entry bookkeeping made simple

Double-entry bookkeeping made simple mostly means this: every movement has two sides, and that is exactly what creates clarity. You do not need to become an accountant first.

If you work with clear examples, collect receipts properly and use workable software, the logic becomes easier surprisingly quickly. Then debit and credit stop feeling like a foreign language and start feeling like structure.

Frequently asked questions about double-entry bookkeeping

Here are short answers to common questions about debit, credit and getting started with double-entry bookkeeping.

What is double-entry bookkeeping in simple terms?

Double-entry bookkeeping means that every business transaction changes two accounts. That is what keeps money movements, assets and liabilities traceable.

What is the difference between simple and double-entry bookkeeping?

Simple bookkeeping focuses more on income and expenses. Double-entry bookkeeping also shows which accounts change on both sides of a posting.

What do debit and credit mean?

Debit and credit are the two sides of every posting. Which side is used depends on the account type and the business case.

Do I need to memorize debit and credit?

Not as a first step. It is more important to understand which account increases and which decreases; confidence with debit and credit usually grows through practice.

Who needs double-entry bookkeeping?

Limited liability companies and corporations use it in practice, while for sole proprietorships and other smaller structures it depends on legal form, turnover and scope.

Is double-entry bookkeeping difficult?

The basic principle is often easier than the terminology around it. With clear examples and a clean structure, getting started becomes much easier.

Can I do double-entry bookkeeping myself?

Yes. Many small businesses can handle it themselves with good routines and suitable software. For special cases or uncertainty, fiduciary support can help selectively.

Is Excel enough?

Maybe for very simple cases. But once invoices, bank reconciliation, VAT or open items enter the picture, Excel quickly becomes cumbersome.

Which software is suitable?

Useful software brings postings, invoices and bank reconciliation together in one clear interface. For beginners, clarity matters more than an oversized feature set.

What happens if I make mistakes?

Mistakes can usually be corrected if they are noticed early. That is exactly why a traceable structure with regular checks matters so much.

What is the easiest way to learn bookkeeping?

The easiest way is through simple practical examples and recurring routines instead of dry definitions. Once the logic behind postings is clear, many things become easier.

Can I start with fibu3 for free?

Yes. You can start with up to 40 entries in fibu3 for free, which makes getting started practical for smaller companies and self-employed professionals.

Approach bookkeeping more clearly

Try fibu3 and start with up to 40 entries for free.