Why accounting terms often seem complicated

Accounting terms often seem complicated because they come from a specific technical language.

Some terms sound similar but mean different things, while others are familiar in everyday language and more precise in bookkeeping.

The 25 most important accounting terms explained simply

1. Bookkeeping

Definition: Bookkeeping is the orderly recording of business events. Example: Company A records an invoice to Customer A and a payment to Supplier B. Important because it creates overview.

2. Supporting document

Definition: A supporting document records a business event in a traceable way. Example: Company A keeps a document for an expense. Important because transactions are easier to understand later.

3. Account

Definition: An account is a collection point for similar transactions. Example: Company A groups several bank movements in one area. Important because similar items stay visible together.

4. Chart of accounts

Definition: A chart of accounts is the structured overview of the accounts in use. Example: Company A uses a selected set of accounts for purchases, sales and bank activity. Important because it creates order.

5. Debit

Definition: Debit is one side of double-entry bookkeeping. Example: Part of a transaction is recorded on the debit side. Important because debit only makes sense together with credit.

6. Credit

Definition: Credit is the second side of double-entry bookkeeping. Example: The matching side of a transaction appears on the credit side. Important because both sides explain the logic.

7. Debtor

Definition: A debtor is a customer with an open receivable. Example: Customer A has received an invoice but not paid yet. Important because expected inflows become visible.

8. Creditor

Definition: A creditor is a supplier or service provider with an open invoice to the business. Example: Supplier B has issued an invoice that is still unpaid. Important because upcoming outflows become visible.

9. Receivable

Definition: A receivable is an open claim for payment. Example: Company A is still waiting for payment from Customer A. Important because future inflows become easier to understand.

10. Liability

Definition: A liability is an open payment obligation. Example: Company A still owes Amount X to Supplier B. Important because liabilities show what still has to be settled.

11. Expense

Definition: Expense describes economic consumption within a period. Example: Company A uses a service from Supplier B. Important because it shows what burdens the business.

12. Revenue

Definition: Revenue describes economic value created within a period. Example: Company A provides a service to Customer A. Important because it shows what supports the business economically.

13. Receipt of money

Definition: A receipt of money is an inflow of funds. Example: Customer A pays Amount X. Important because it matters for liquidity.

14. Payment

Definition: A payment is an outflow of funds. Example: Company A pays Amount Y to Supplier B. Important because it sharpens the view on cash movement.

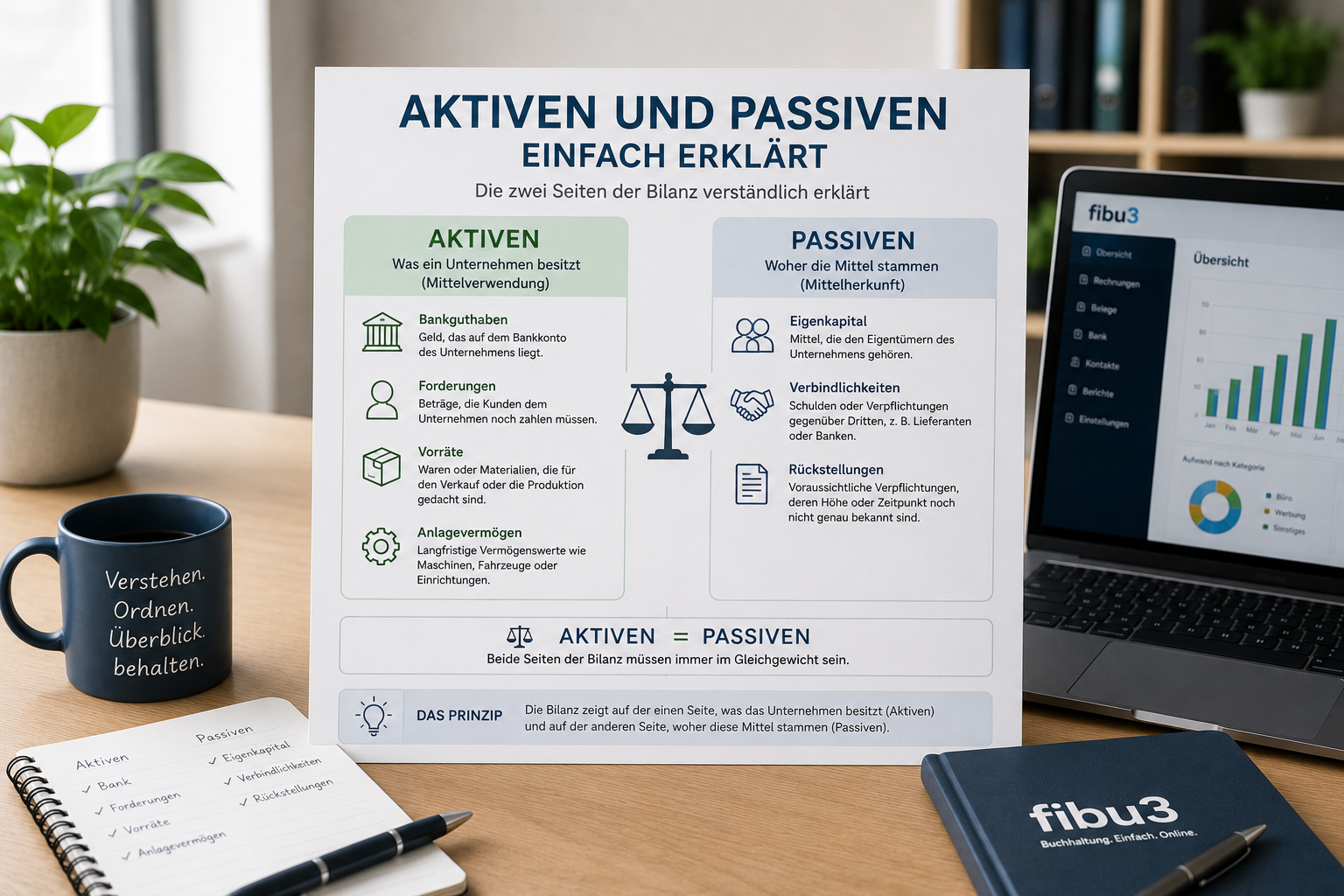

15. Balance sheet

Definition: The balance sheet shows the financial position at a specific point in time. Example: Company A sees its values and how they are financed. Important because it shows structure and position.

16. Assets

Definition: Assets are the values of a business. Example: Company A has bank balances, receivables or work equipment. Important because assets show what belongs to the business.

17. Liabilities and equity side

Definition: This side shows how assets are financed. Example: Company A shows equity and open obligations there. Important because the origin of capital becomes visible.

18. Equity

Definition: Equity is the capital attributable to the business itself. Example: Company A has equity from contributions and results. Important because it describes the company’s own base.

19. Outside capital

Definition: Outside capital comes from outside parties and remains to be settled or repaid. Example: Company A has obligations towards third parties. Important because it shows external financing.

20. Income statement

Definition: The income statement compares revenue and expense for a period. Example: Company A sees economic contributions and burdens over time. Important because it explains development.

21. Fixed assets

Definition: Fixed assets are values used over a longer period. Example: Company A uses Asset B across several periods. Important because they are not only short-term items.

22. Current assets

Definition: Current assets are values connected more closely with day-to-day operations. Example: Company A has cash, bank balances or receivables. Important because they matter for everyday business.

23. Depreciation

Definition: Depreciation reflects that a longer-used asset loses significance over time. Example: Company A uses Asset B over several periods. Important because the time dimension becomes visible.

24. Liquidity

Definition: Liquidity describes whether a business can make its ongoing payments on time. Example: Company A waits for payments from Customer A and watches available funds. Important because it focuses on available money.

25. Bank reconciliation

Definition: Bank reconciliation means matching bookkeeping with bank movements. Example: Company A checks whether a payment from Customer A is also visible on the account. Important because gaps become visible.

Which terms are mixed up most often?

Expense vs. payment

Expense is an economic burden, payment is an outflow of money.

Revenue vs. receipt of money

Revenue is economic value creation, receipt of money is an inflow of funds.

Debtor vs. creditor

Debtors relate to customer receivables, creditors to supplier invoices.

Balance sheet vs. income statement

The balance sheet shows a point in time, the income statement a period.

Liquidity vs. profit

Liquidity is available money, profit is economic success.

How does fibu3 help keep the overview?

fibu3 helps make accounting terms less abstract in daily work because invoices, payments and bookkeeping stay visible in one structure.

This article is for educational and informational purposes only.

In short – accounting terms

Accounting terms are the language of bookkeeping. Understanding the most important terms makes it much easier to follow transactions, documents and reports.

Related topics

Conclusion

Many accounting terms are easier than they first appear. Understanding the core terms makes bookkeeping more readable.

Frequently asked questions about accounting terms

Short answers to common questions about core accounting terms. The answers are for general information only.

Which accounting terms should I know?

Helpful core terms include document, account, debit, credit, debtor, creditor, expense, revenue, balance sheet, income statement, liquidity and bank reconciliation.

What is the difference between expense and payment?

Expense is an economic burden, while a payment is an outflow of money. The two can occur together but do not have to.

What is the difference between revenue and receipt of money?

Revenue describes economic value creation, while a receipt of money describes an inflow of funds.

What is the difference between debtor and creditor?

Debtors relate to customer receivables. Creditors relate to supplier or service invoices.

What do debit and credit mean?

Debit and credit are the two sides of double-entry bookkeeping and together represent a business transaction.

What is a balance sheet?

A balance sheet shows the financial position of a business at a specific point in time.

What is an income statement?

An income statement shows the revenue and expense of a business over a period.

What does liquidity mean?

Liquidity describes whether a business can make its ongoing payments on time.

What is a supporting document?

A supporting document records a business event in a traceable way and helps make it understandable later.

Why is bank reconciliation used?

Bank reconciliation helps compare bookkeeping with bank movements and makes links between them easier to understand.

Which software helps with the overview?

Helpful software brings invoices, payments, records and bookkeeping together in one clear structure.

Can fibu3 help with this?

Yes. fibu3 helps document business events clearly and makes terms easier to understand in practice.

Related fibu3 solutions

Keep bookkeeping, invoices and payments easier to understand

With fibu3, business events, invoices and payments stay in one clear structure, making accounting terms easier to understand in daily work.