Depreciation explained simply

Many people hear the word depreciation and immediately think of complicated bookkeeping. In reality, the basic principle is simple.

This article is for educational and informational purposes only. You do not need prior knowledge. The examples below deliberately use general roles and placeholders such as Amount X, Amount Y, Asset A and Asset B.

The goal is to explain what loss in value means, why depreciation appears in bookkeeping and why depreciation does not mean paying money again.

What is depreciation?

Depreciation describes, in simplified terms, the loss in value of an asset over time.

An asset or work tool is often used by a company for a longer period. Over time, its value changes because of use, ageing, wear or technical progress.

Bookkeeping makes this change visible. Depreciation in bookkeeping is therefore not a mysterious special rule, but a way to document loss in value.

Why does depreciation exist?

Depreciation exists so that assets do not appear in bookkeeping as if they always kept exactly the same value.

If a company uses an asset over a longer period, its economic significance changes over time. Depreciation helps document that development in an orderly way.

This makes bookkeeping easier to understand because assets are shown more realistically and changes remain traceable.

- Changes in value become visible.

- Bookkeeping remains easier to follow.

- Purchases and ongoing use are easier to classify.

- The overview of assets becomes clearer.

What is often depreciated?

Typical examples are purchases that a company uses over a longer period and does not consume or resell immediately.

The following overview shows common categories. This example is only meant to explain the basic principle.

| Category | Example |

|---|---|

| Work equipment | Asset A that is used in day-to-day business over a longer period. |

| Vehicles | Vehicles used for operational trips or assignments. |

| Machines | Machines or production equipment that serve the business over time. |

| Fixtures | Furniture, fittings or fixed equipment for the business. |

| Technical devices | Devices, systems or technical infrastructure for daily work. |

| Intangible assets | Usage rights, software or other non-physical assets. |

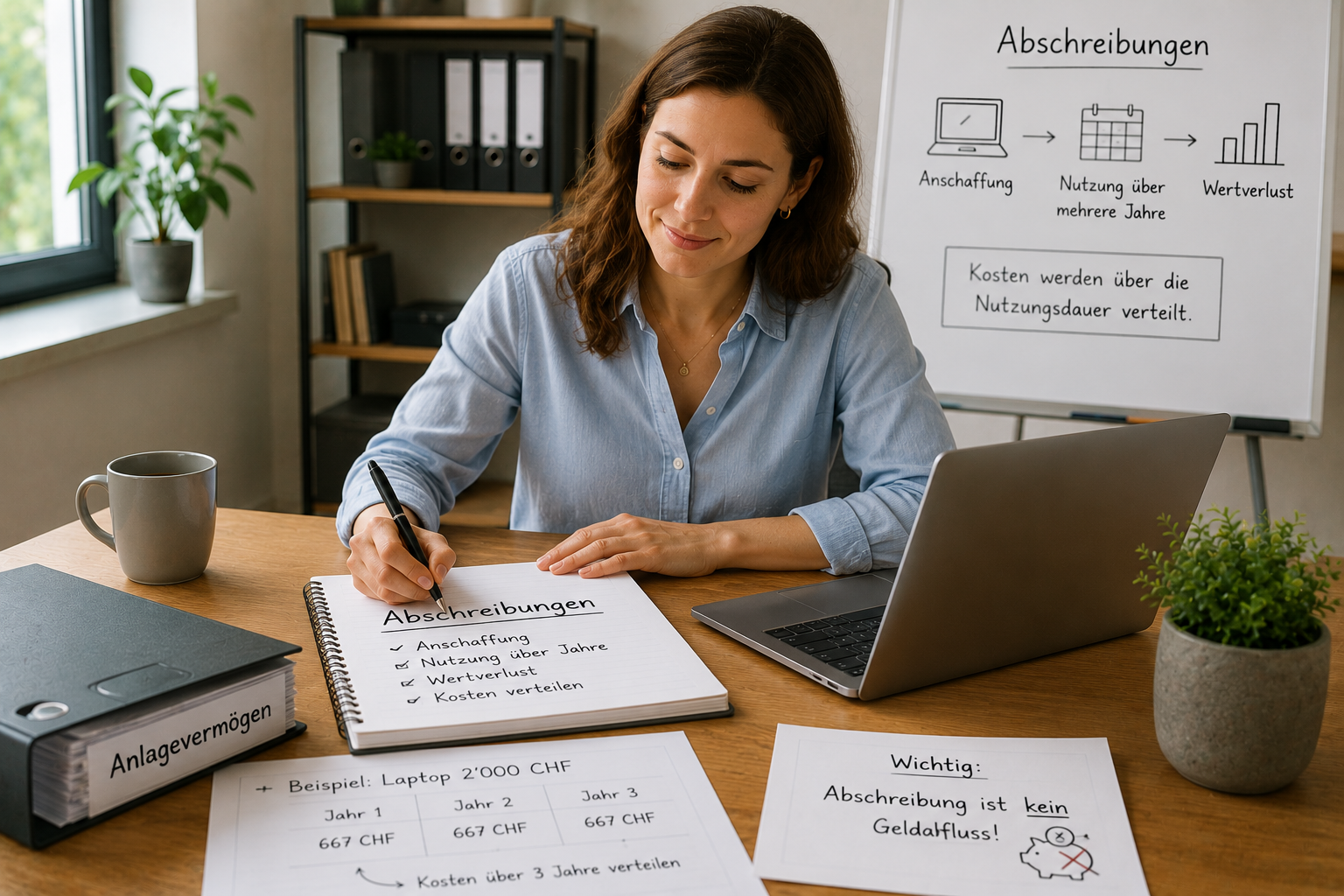

Simple practical example

A company buys Asset A for Amount X. The asset is not used only briefly, but remains part of the business for a longer period.

The cash outflow happens when the company buys it. After that, the asset stays in the business and its value changes over time.

That change appears in bookkeeping because the loss in value should not remain invisible.

This example is only meant to explain the basic principle.

Basic idea

- A company acquires Asset A for Amount X.

- The asset is used over a longer period.

- Its value changes over time.

- Bookkeeping reflects that change through depreciation.

Does depreciation mean cash outflow?

No. Depreciation does not mean that money is paid again.

Payment and depreciation are two different things. The money flows when the purchase is made. Depreciation appears later in bookkeeping because the asset changes in value over time.

For bookkeeping beginners, this is the key point: depreciation is not a second invoice and not a new payment, but a bookkeeping representation of loss in value.

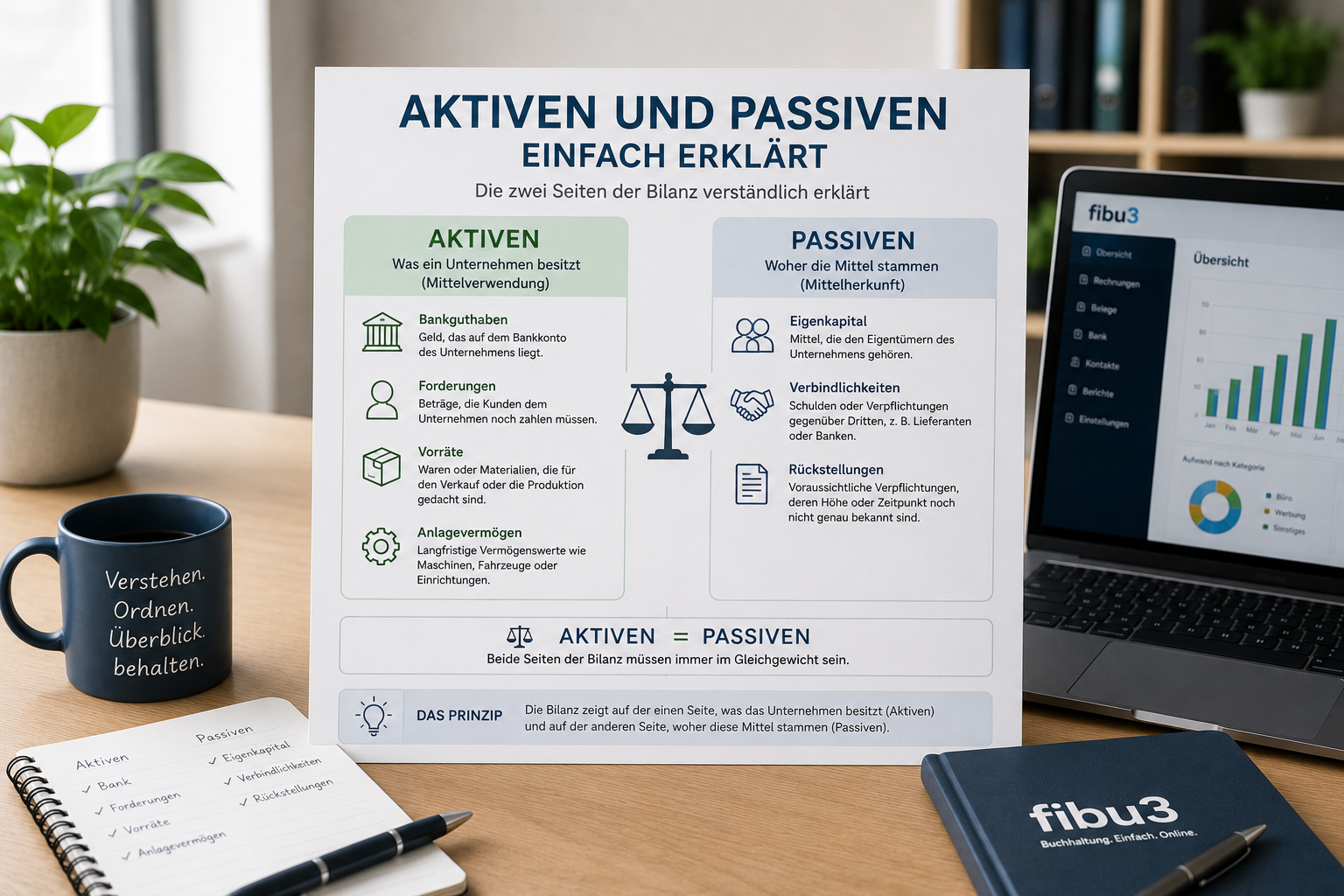

What are fixed assets?

Fixed assets are assets a company uses over a longer period and does not hold for direct resale.

They often include work equipment, fixtures, technical devices or Asset B that remains in the business over time.

Fixed assets explained simply means values that are meant to serve the business instead of disappearing immediately.

Why does depreciation appear in bookkeeping?

Depreciation appears in bookkeeping because bookkeeping does not only record payments, but also changes in assets.

If an asset loses value over time, that development should not remain hidden. Depreciation makes it visible.

This helps explain how investments, use and value changes fit together in a business.

Typical misunderstandings about depreciation

Many misunderstandings do not come from complicated rules, but from mixing different topics together.

Confusing depreciation with payment

The purchase triggers the cash outflow. Depreciation later describes the change in value.

Treating depreciation as tax savings

This article explains the bookkeeping principle, not individual tax effects.

Treating every loss in value the same way

Not every change is recorded in exactly the same way. The concrete treatment can vary depending on the situation.

Confusing fixed assets with consumables

Assets used over time are something different from items that are consumed immediately.

How does fibu3 help keep track?

fibu3 helps document business events and investments in a structured way.

In practice, that means recording acquisitions, keeping postings traceable, storing documents in an orderly way and maintaining a clearer overview of assets.

That is especially helpful when a business wants not only to understand value changes, but also to document them cleanly.

In short - depreciation

Depreciation describes, in simple terms, the loss in value of an asset over time. It shows in bookkeeping how the value of a longer-used asset changes, without causing a new cash outflow.

Checklist

If you can answer these questions mostly with yes, you already understand the basic principle well.

- Yes/No: Do I understand the difference between payment and depreciation?

- Yes/No: Do I know what fixed assets are?

- Yes/No: Do I document investments clearly?

- Yes/No: Do I have an overview of my assets?

- Yes/No: Do I understand why loss in value appears in bookkeeping?

Related topics

If you now understand depreciation explained simply, these topics are a useful next step.

Conclusion: depreciation explained simply

Depreciation explained simply means above all that an asset does not keep exactly the same value forever, and bookkeeping makes that change visible.

Once you understand the difference between payment and loss in value, it becomes much clearer why depreciation appears. This article is intended as neutral educational guidance. The concrete treatment can vary depending on the situation.

Frequently asked questions about depreciation

Short answers to common questions about depreciation, loss in value, fixed assets and bookkeeping. The answers are for general information only.

What is depreciation?

Depreciation describes, in simplified terms, the loss in value of an asset over time.

Why does depreciation exist?

So that changes in assets remain visible in bookkeeping and values do not appear permanently unchanged.

What does loss in value mean?

It means that an asset is no longer economically worth exactly the same amount over time as it was at the beginning.

What are fixed assets?

Fixed assets are assets a company uses over a longer period and does not hold for direct resale.

Does depreciation mean payment?

No. Payment happens when the purchase is made. Depreciation later describes the change in value.

Why does depreciation appear in bookkeeping?

Because bookkeeping shows not only payments, but also changes in assets.

What is often depreciated?

Typical examples are work equipment, vehicles, machines, fixtures, technical devices or intangible assets used over a longer period.

Why are devices and machines mentioned?

Because such purchases are often used over time in the business and are therefore typically linked to changes in value.

What mistakes happen frequently?

A common mistake is confusing depreciation with payment or not distinguishing clearly between fixed assets and consumables.

How do I keep track?

Helpful elements are clear documentation, orderly records and an ongoing overview of purchases and assets.

Which software helps?

Helpful software brings together acquisitions, bookkeeping entries and documents in a traceable way.

Can fibu3 support this?

Yes. fibu3 helps document business events, investments and documents clearly.

Related fibu3 solutions

Document investments clearly

With fibu3, acquisitions, bookkeeping entries and documents stay in one place so business events are easier to track.