What is a year-end closing?

A year-end closing summarizes the financial position of a business at the end of a financial year. Put simply, it shows what came in, what went out and where the business stands financially.

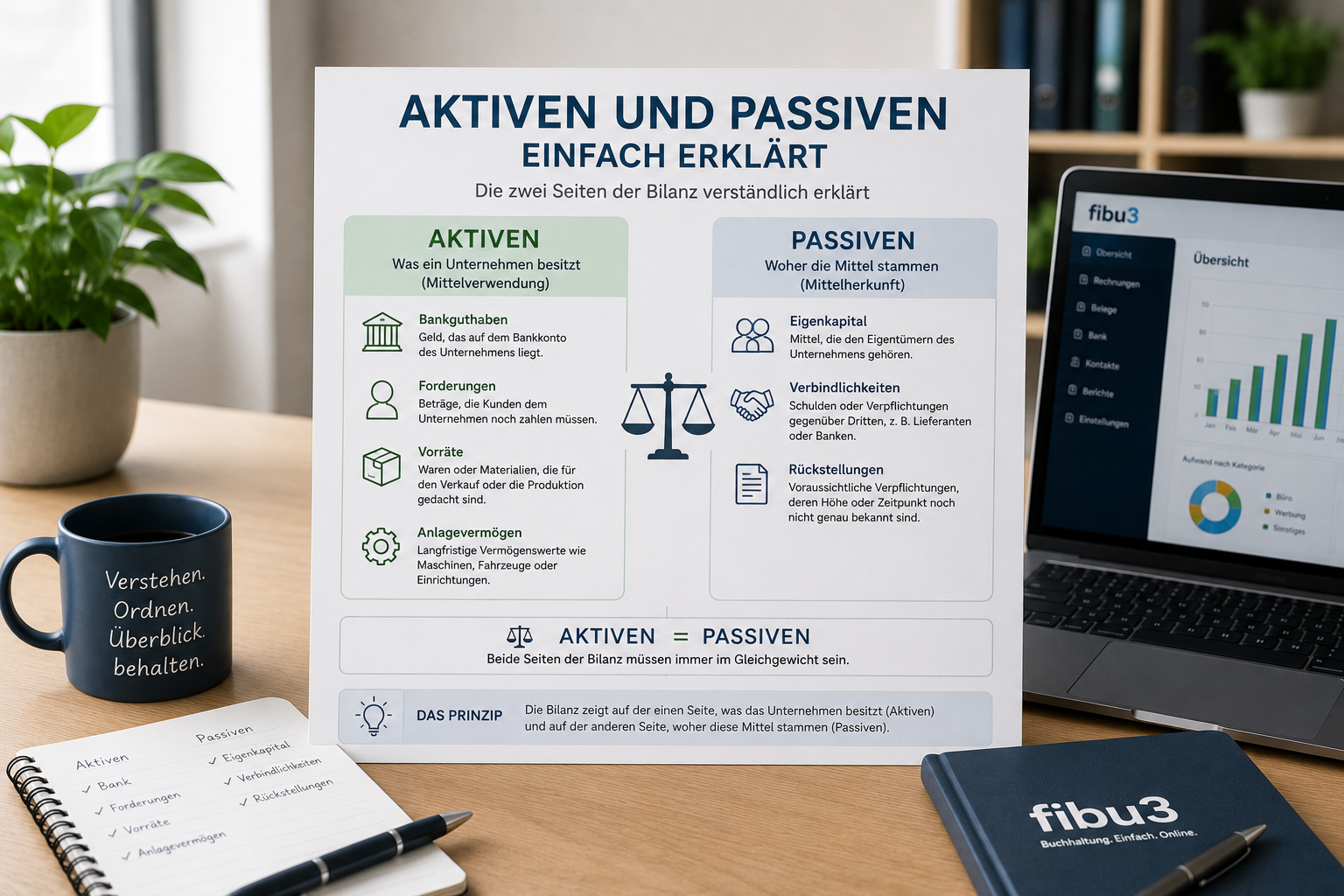

For many Swiss SMEs, the annual financial statements consist of a balance sheet and an income statement, depending on legal form and size with additional information. The balance sheet shows assets, liabilities and equity at a date. The income statement shows revenue, expenses and the result for the year.

In practice, year-end closing is not only an exercise for taxes or fiduciaries. It is also a reality check: do bank balances, open invoices, VAT, private shares and documents match the ongoing bookkeeping?

Who needs a year-end closing in Switzerland?

In Switzerland, many businesses must keep their accounts so that a traceable closing is possible at year end. Legal entities such as limited companies and corporations generally keep regular accounts with balance sheet and income statement.

Sole proprietorships and partnerships below CHF 500,000 turnover may often use simplified bookkeeping. Even then, they need a clean view of income, expenses and assets so that tax return and business figures are correct.

Associations differ depending on size, statutes, financing and activity. If an association keeps accounts, the closing should also be prepared cleanly. If in doubt, check current rules or speak with your fiduciary.

Year-end closing checklist - step by step

Year-end closing in Switzerland becomes much calmer when you do not leave the preparation until the final week. This checklist is deliberately practical.

Are all receipts complete?

Check whether every business expense has a document. Missing receipts cost a lot of time at closing because entries become hard to trace.

Check open invoices

Review all customer invoices that are unpaid at year end. Open items must be clear, otherwise revenue, receivables and liquidity planning become unreliable.

Control incoming payments

Compare incoming payments with open invoices. This reveals duplicate payments, wrong allocations or invoices that still need a reminder.

Reconcile the bank account

The bank account in bookkeeping should match the bank statement. Differences often point to missing entries, duplicates or wrongly allocated payments.

Check credit cards and cash

Business credit cards, cash and payment providers are easily forgotten. Collect statements and make sure fees, refunds and cash expenses are recorded.

Review VAT

If you are VAT-registered, review turnover, input tax, private shares and corrections. If closing and VAT returns do not align, questions arise later.

Review private shares

Mixed expenses such as vehicle, phone, home office or meals should be assessed cleanly. If unsure, a short fiduciary check is often worthwhile.

Review depreciation

Larger purchases are not always posted directly as expenses. Check which assets exist and whether depreciation is treated correctly.

Review debtors and creditors

Debtors are open customer receivables, creditors are open supplier invoices. Both lists should be current and free of old unexplained items.

Prepare documents for tax or fiduciary

File bank statements, invoices, receipts, contracts, payroll documents and VAT papers in order. Better preparation means fewer questions.

Which documents do I need?

You do not need a textbook-perfect archive. You need complete, traceable records where figures and documents fit together.

| Document | Why it matters |

|---|---|

| Bank statements | They show whether bookkeeping matches actual account movements. |

| Invoices | Outgoing and incoming invoices explain revenue, expenses, receivables and liabilities. |

| Receipts | Receipts, expenses and payment proofs make entries traceable. |

| Contracts | Rent, leasing, loans or subscriptions explain recurring payments and obligations. |

| Cash overview | For cash, it must be clear what was received, spent and available at year end. |

| VAT documents | For VAT-registered businesses, returns, reconciliations and corrections are central. |

| Payroll documents if relevant | Wages, social insurance and withholding tax must match bookkeeping. |

Which mistakes happen often?

Most mistakes do not happen because bookkeeping is extremely complicated. They happen because documents are collected too late or checks are postponed too long.

- Missing receipts: an entry without a document is hard to explain later.

- Bank account not reconciled: small differences can trigger many follow-up questions.

- VAT forgotten: mistakes in input tax, rates or turnover reconciliation are often found late.

- Open invoices ignored: receivables and liabilities must be visible at the reporting date.

- Everything left until the last moment: time pressure leads to estimates, questions and stress.

- Private and mixed expenses posted incorrectly: sole proprietorships in particular need a clear separation.

- Excel chaos: several versions, manual formulas and missing documents make closing unnecessarily difficult.

How do you avoid stress before deadlines?

The simplest way is a small rhythm during the year. If you reserve 30 to 60 minutes every month for receipts, bank reconciliation and open invoices, there is much less to clean up at closing.

Do not wait until the fiduciary asks for everything. Create a list of open questions early: unclear expenses, larger purchases, private shares, VAT corrections or payroll topics. Such points are easier to clarify calmly than shortly before a filing deadline.

A fixed closing folder also helps, digital or physical. It should contain bank statements, VAT returns, important contracts, payroll documents, inventory lists and larger receipts. At year end, you do not have to search through emails, downloads and several Excel versions.

- File receipts monthly and request missing documents immediately

- Reconcile the bank regularly instead of only in January

- Check open customer invoices before year end

- Mark unclear postings during the year and clarify them deliberately

- Hand documents to the fiduciary in a structured way, not as a loose collection

What can I do myself - and when does a fiduciary help?

Businesses can do many preparatory tasks themselves. A fiduciary becomes especially useful when tax, legal or more complex questions arise.

This is not an either-or decision. Often the best way is: you keep ongoing bookkeeping clean, the fiduciary reviews closing, taxes and special cases.

| Do yourself | Fiduciary useful |

|---|---|

| Collect and file receipts | Assess special cases and tax questions |

| Reconcile the bank regularly | Review or prepare year-end closing |

| Check invoices and incoming payments | Tax return and tax planning |

| Control open items | VAT corrections, private shares and accruals |

| Look at simple reports | Payroll, depreciation and complex account allocation |

| Prepare structured documents | Change of legal form, financing or growth situations |

How does fibu3 help with year-end closing?

fibu3 helps you keep ongoing bookkeeping in a way that year-end closing does not start from zero. Invoices, documents, postings and bank reconciliation sit closer together in one interface.

You can create invoices, control incoming payments, reconcile bank movements and record postings in a more structured way. This does not replace a fiduciary, but it makes preparation much cleaner.

When a fiduciary reviews the closing, good data is valuable. Less searching, fewer unexplained entries and clearer reports mean the specialist can focus more on review and special questions.

In short: year-end closing in one sentence

Year-end closing shows at the end of a financial year what a business has earned, which assets and liabilities exist, and whether bookkeeping, documents, bank and taxes fit together in a traceable way.

Year-end readiness check - are you ready?

If you can answer most of these questions with yes, your closing is well prepared. If several points are open, it is worth cleaning up early.

- Are all receipts available?

- Is your bank account reconciled?

- Have you checked open invoices?

- Are debtors and creditors up to date?

- Has VAT been reviewed if relevant?

- Are private and business expenses separated?

- Are documents for tax or fiduciary organized?

- Do you know where you need professional help?

Conclusion: year-end closing in Switzerland without unnecessary stress

A clean year-end closing in Switzerland does not have to be complicated. What matters is that receipts, bank, invoices, VAT and open items are maintained during the year and do not appear shortly before the deadline.

You can prepare many routine tasks yourself. For review, taxes, VAT special cases or complex structures, a fiduciary is a useful specialist. Good preparation saves time, reduces questions and gives you a better view of your figures.

Related topics

Useful internal topics for links: VAT explained simply, do your own bookkeeping, double-entry bookkeeping, simplified bookkeeping, writing invoices, bank reconciliation, prices, learn and blog.

Frequently asked questions about year-end closing in Switzerland

Short answers about documents, preparation, fiduciaries, Excel and software.

What belongs to year-end closing?

Depending on the business, year-end closing includes balance sheet, income statement, open items, documents, bank reconciliation and tax-relevant records. The key is traceability.

When do I need to do year-end closing?

It is normally done after the financial year ends, often as of 31 December. Exact tax and filing deadlines depend on canton, legal form and situation.

What do I need for year-end closing?

You need bank statements, invoices, receipts, contracts, cash overview, VAT documents and payroll records if you have employees.

Can I prepare year-end closing myself?

Yes. Collecting receipts, checking invoices, reconciling the bank and organizing documents can be handled by many businesses themselves.

Do I need a fiduciary?

Not for every routine task. A fiduciary is useful for closing review, taxes, VAT special cases, payroll or more complex structures.

Which mistakes happen often?

Common issues are missing receipts, unreconciled bank accounts, VAT checked too late and forgotten open invoices.

How should I prepare?

Work monthly or quarterly: file receipts, reconcile the bank, review open invoices and clarify unclear postings early.

Is Excel enough?

For very simple cases Excel can be enough. With regular invoices, VAT, several accounts or growth, software is usually more reliable.

What should I check?

Check bank, cash, credit cards, debtors, creditors, VAT, private shares, depreciation and completeness of documents.

What is the difference between bookkeeping and year-end closing?

Bookkeeping records business transactions during the year. Year-end closing summarizes, checks and presents the financial situation at year end.

Can fibu3 help?

Yes. fibu3 helps prepare invoices, postings, documents and bank reconciliation more cleanly, so closing and fiduciary review become less chaotic.

Can I start with fibu3 for free?

Yes, you can start with up to 40 postings free of charge and see whether fibu3 fits your daily work.

Prepare year-end closing better

With fibu3, invoices, postings and bank reconciliation stay more organized, so you or your fiduciary can review year-end closing more calmly.